Most retail investors own the market. They buy a broad index fund, hold it, and accept whatever return the market delivers. That approach is sound, but it is not the only evidence-based option available.

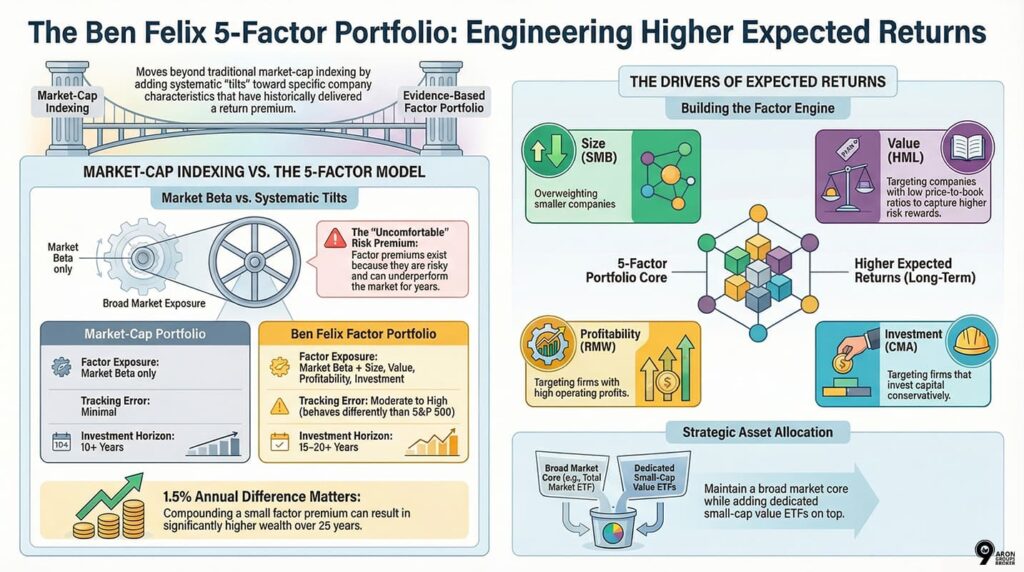

The Ben Felix portfolio extends standard index investing by adding systematic exposure to four additional return factors: size, value, profitability, and investment.

Each factor boasts a long academic history and a plausible economic explanation. Decades of data support their positive return premium—the extra historical return above the market.

- The Ben Felix portfolio applies academic factor research to real-world asset allocation, not speculation.

- Holding more factors than market beta alone has historically widened the range of expected returns.

- Factor premiums are not guaranteed; they appear across long periods and can disappear for years.

- Low-cost ETFs remain the most practical vehicle for building a systematic factor portfolio.

Foundations of the Ben Felix Portfolio

This section explores how evidence-based research and systematic tilts move beyond traditional indexing to target specific drivers of long-term returns.

The Origins of the Model at Rational Reminder and PWL Capital

Ben Felix is a portfolio manager at PWL Capital, a Canadian firm focused on evidence-based investing. He also co-hosts the Rational Reminder podcast. This show explains academic financial research and applies it to real-world portfolio building.

The Ben Felix model portfolio grew from this research-first culture. It is not a secret product you must buy. Instead, it is a transparent framework based on the Fama-French five-factor model. This is one of the most respected models in financial history.

Both the Rational Reminder community and PWL Capital openly share these methods. This makes the PWL Capital model portfolio a clear guide for any retail trader looking for professional factor exposure.

Key Point:

The Ben Felix portfolio is not a fund you buy directly. It is an allocation framework you implement yourself using low-cost ETFs or ETF CFDs.

Evidence-Based Investing and Systematic Factor Exposure

Evidence-based investing means choosing a strategy because scientific, peer-reviewed research supports it. You do not pick it because it performed well last month.

The Ben Felix portfolio uses this principle to target factor premiums. These are specific drivers of returns that have persisted across many decades and global markets.

Systematic factor exposure means holding a rules-based “tilt” toward certain types of stocks. Instead of picking individual companies, you buy funds that focus on characteristics like:

- Small Company Size: Targeting firms with lower market values.

- Low Price-to-Book: Buying stocks that are cheap relative to their assets.

This approach removes emotional decision-making from your trading. The strategy is set in advance. You only make changes when your rebalancing thresholds are crossed.

Q: If these factors are supported by “science,” why don’t they work all the time?

A: Factor premiums exist because they are risky; if they outperformed constantly, they would be “arbitraged away” as prices rose to meet demand. Their “uncomfortable” nature during market stress is exactly why they offer higher expected returns to the disciplined investors who provide them with capital.

How the Ben Felix Portfolio Differs from Market-Cap Indexing

A standard market-cap index fund, like one tracking the MSCI World, holds stocks based on their total market value. Larger companies receive greater weight in the fund. This means your portfolio earns the market beta, which is a return that moves in line with the general stock market.

The Ben Felix portfolio keeps that broad market exposure but adds deliberate tilts. It specifically targets:

- Smaller companies (Size factor);

- High profitability (Quality factor);

- Low valuations (Value factor);

- Conservative investment patterns (Investment factor).

These tilts introduce additional risk factors. Historically, each of these factors has carried its own return premium. This means you are taking on specific risks to seek higher expected returns over time.

The practical result is a portfolio that behaves differently from a plain index fund. It will sometimes outperform and sometimes underperform the market. This depends entirely on which factor investing strategies are currently in or out of favour.

The Fama-French Five-Factor Model in Practice

Understand the academic mechanics behind size, value, and profitability premiums to see how they function as distinct risk rewards in a portfolio.

Size, Value, Profitability, and Investment Factors Explained

The Fama–French five-factor model (developed by Eugene Fama and Kenneth French) identifies five sources of systematic equity returns. Each factor is defined by a measurable characteristic of a company’s shares.

| Factor | What It Measures | Premium Logic |

|---|---|---|

| Market beta | Sensitivity to overall market returns | Compensation for holding risky equities |

| Size (SMB) | Small companies vs large companies | Small firms carry a higher business risk |

| Value (HML) | Low price-to-book vs high price-to-book | Distressed firms demand higher expected returns |

| Profitability (RMW) | High operating profit vs low | Profitable firms sustain earnings more reliably |

| Investment (CMA) | Conservative investment vs aggressive | Firms that invest cautiously tend to return more capital |

- SMB = Small Minus Big;

- HML = High Minus Low;

- RMW = Robust Minus Weak;

- CMA = Conservative Minus Aggressive.

Key Point:

Each of the five factors is a long-short portfolio in academic theory. In practice, you gain factor exposure by overweighting securities with the desired characteristics, not by shorting.

Risk Premia and Market Beta in Expected Returns

- A risk premium is the extra return you expect for taking a specific type of risk. It is the reward for choosing risky assets over “safe” ones like government bonds.

- Market beta is the most common risk premium. By owning shares instead of bonds, you accept market volatility. Historically, the market has rewarded investors for taking this risk.

The Ben Felix 5-factor portfolio adds 4 more risk premia on top of market beta. Each premium might seem small in a single year. However, when compounded over decades, the impact on your total returns is significant.

It is vital to understand that a risk premium is expected, not guaranteed. If a factor had no risk of losing money, everyone would buy it. This would cause the extra profit to disappear.

Why Factor Strategies Experience Cycles of Underperformance

Factor investing strategies often go through long periods where a specific factor delivers lower returns than the broader market. These cycles are a natural part of investing and can last over a decade.

Between 2007 and 2020, value investing experienced its most challenging period since World War II. Data from J.P. Morgan and CFA Society Netherlands highlight this “lost decade”:

- Annual Underperformance: Value stocks trailed growth stocks by approximately 4.3% per year from 2007 to March 2020.

- Massive Drawdown: The Fama-French value factor suffered a 55% drop relative to growth during this timeframe.

- Global Impact: This trend was seen across almost all geographic regions and industry sectors.

These cycles do not mean a factor is “dead.” Instead, they prove that the factor carries genuine risk. If value stocks always outperformed, they wouldn’t be risky, and the extra return would disappear.

Investors who sell during a drawdown lock in these losses and miss the sharp recovery that often follows.

Warning:

The value factor underperformed growth for over 10 years before recovering sharply in 2021-2022. Investors who quit early missed the entire recovery.

Strategic Asset Allocation Framework

Building a strong strategy requires balancing equities and bonds while ensuring broad geographic diversification to manage global market risks effectively.

Equity-Bond Allocation Based on Risk Tolerance

The first decision in building any portfolio is the split between equities (shares) and bonds.

- Equities: These provide long-term growth by capturing various risk premia.

- Bonds: These provide stability and reduce drawdowns when the stock market falls.

The right allocation depends on your investment timeline and your psychological ability to handle losses. A common starting point for long-term investors is 80% equities and 20% bonds. However, you must adjust this to your own life goals and financial needs.

| Allocation Type | Risk Level | Primary Goal |

|---|---|---|

| 100% Equity | Very High | Maximum Growth |

| 80/20 Mix | High | Growth with some Cushion |

| 60/40 Mix | Moderate | Balanced Growth and Safety |

PWL Capital model portfolio documents provide clear guidance for different risk profiles. You should review these resources alongside professional financial advice before you set your final target weights.

Important:

Asset allocation explains more of your long-term return than picking individual "winning" stocks. This is the most important decision you will make.

Diversification Across Developed and Emerging Markets

The Ben Felix portfolio achieves global diversification by holding stocks across different regions. This reduces your risk because you are not tied to a single country’s economy.

The portfolio generally splits investments into two main categories:

- Developed Markets: Stable economies like North America, Europe, and Japan.

- Emerging Markets: Faster-growing economies like China, India, and Brazil.

Emerging markets carry extra risks, such as currency volatility and political uncertainty. However, they also offer a higher expected return. This aligns perfectly with the overall strategy’s risk-premium logic.

A typical Ben Felix portfolio allocation holds a smaller weight in these regions. Most investors allocate between 10% and 15% of their total portfolio (or 20-30% of their equity portion) to emerging markets. This balance captures growth while managing high volatility.

Integrating Size and Value Tilts Within Asset Allocation

The Ben Felix portfolio does not replace the whole market. Instead, it “overweights” specific areas. This means you hold more small-cap and value stocks than a standard index fund would.

To do this, you keep a broad market ETF as your foundation and add dedicated small-cap value ETFs on top.

This strategy does not eliminate large companies or growth stocks. It simply shifts your factor investing strategies to capture specific premiums. You get the best of both worlds:

- Broad Diversification: The safety of the global stock market.

- Factor Loading: The higher expected return from smaller, cheaper companies.

| Component | Purpose | Examples |

|---|---|---|

| Core Holding | Tracks the total global market | MSCI World, S&P 500 |

| Factor Tilt | Adds exposure to Size and Value | Russell 2000, Value ETFs |

The result is a Ben Felix portfolio allocation that mostly follows the global market but has the potential for incremental gains over long periods.

Q: Does adding a Small-Cap Value tilt increase my exposure to specific sectors like Tech or Energy?

A: Yes, significantly. A broad market index like the S&P 500 is currently dominated by Growth (Tech/Software). By adding a Value tilt, you are intentionally shifting your weight toward sectors like Financials, Industrials, and Energy, which typically trade at lower price-to-book ratios. This creates “sector diversification” that protects you if high-flying tech valuations suddenly contract.

ETF Selection and Smart Beta Implementation

Discover how to identify high-quality, low-cost “smart beta” funds that accurately track factor indices while maintaining high liquidity and tax efficiency.

Choosing Low-Cost Global Equity and Bond ETFs

The foundation of the Ben Felix ETF portfolio is a set of low-cost, diversified global equity and bond ETFs. You must check the Total Expense Ratio (TER). This is the annual cost of holding a fund. Costs compound against your returns, so keeping them low is vital.

Common options for global equity exposure include funds tracking these indices:

- MSCI World (Developed markets only)

- MSCI All Country World Index (ACWI) (Includes emerging markets)

- FTSE All-World (Broad global coverage)

For bonds, funds tracking the Bloomberg Global Aggregate Bond Index offer broad diversification.

The specific funds available to you depend on your country and local tax laws. Always verify the tax implications before you buy.

Key Point:

A cost difference of only 0.50% per year may seem small. Over 30 years, compounding turns that small fee into a massive loss in your final portfolio value.

Small Cap Value ETFs and Russell 2000 as a Size Proxy

To use the size and value factors, the Ben Felix model portfolio adds small-cap value ETFs to your broad equity holdings. These funds filter the market for companies that are:

- Small: Lower market capitalisation than the average firm.

- Cheap: Lower price-to-book ratios than the average firm.

The Russell 2000 index is a famous proxy for US small-cap stocks. It tracks the 2,000 smallest companies in the Russell 3000 index. However, the Russell 2000 is not a pure “value” fund. To be more precise, Ben Felix often suggests dedicated small-cap value funds or Dimensional Fund Advisors (DFA) strategies.

For exposure outside the US, you can use funds tracking the MSCI World Small Cap Value index. These regional indices help extend your factor tilt to international markets.

Smart Beta Structures for Targeted Factor Exposure

Smart beta refers to ETFs that do not use standard market-cap weighting. Instead, they use rules-based screens to select and weight stocks. These screens include:

- Value ratios: Looking for cheap stock prices.

- Profitability metrics: Finding companies with high earnings.

- Investment rates: Tracking how companies spend their capital.

Smart beta funds sit between standard index funds and active management. They are transparent and rules-based, but they target specific factors. This makes them perfect tools for the Ben Felix 5-factor portfolio.

When choosing a smart beta fund, look for:

- TER: Keep annual costs low.

- Methodology: Ensure it truly targets the factor you want.

- Liquidity: Check that it is easy to buy and sell.

- Tracking Consistency: See if it follows its index accurately.

Using ETF CFDs on MT5 for Flexible Portfolio Access

A Contract for Difference (CFD) on an ETF lets you trade price movements without owning the actual fund. On the MT5 platform, ETF CFDs cover a wide range of global equity, bond, and sector funds.

This structure is helpful for retail traders who want a factor-diversified portfolio in one account. It is especially useful if direct ETF ownership is restricted in your region. MT5 also allows for automated orders, which helps with disciplined rebalancing.

However, CFDs have extra costs, such as overnight financing charges (swap rates). You must evaluate these fees carefully before using CFDs for long-term strategies.

Constructing the Ben Felix Portfolio Step by Step

Follow a clear technical process to define your investment policy, evaluate fund candidates, and execute trades efficiently on the MT5 platform.

Setting Target Weights Aligned with Investment Objectives

Before you buy any fund, define your target allocation in writing. This document, your investment policy statement, should clearly list:

- Your equity-bond split.

- Your geographic allocation.

- Your specific factor tilts.

- The rebalancing rules you will follow.

Below is a representative Ben Felix portfolio allocation. This is a starting point for a long-term investor with a high risk tolerance. These weights are illustrative and not personalised advice.

| Allocation Type | Approximate Weight |

|---|---|

| Global Developed Market Equities (Broad) | 40% |

| Global Small-Cap Value Equities | 25% |

| Emerging Market Equities | 15% |

| Global Government and Aggregate Bonds | 20% |

Adjust these percentages based on your own risk tolerance, time horizon, and tax situation before you start.

Evaluating Funds by Cost, Liquidity, and Tracking Error

Once your target weights are set, judge potential funds using three main criteria:

- Cost (TER): A higher Total Expense Ratio costs you more every year for the same exposure.

- Liquidity: Check the daily trading volume and the bid-ask spread. Low liquidity makes it harder to buy or sell at a fair price, raising your transaction costs.

- Tracking Error: This shows how closely a fund follows its index. High tracking error means the fund is failing to provide the specific factor exposure you planned for.

Identify two or three candidate funds for each category. Compare them using these three points before making your final choice.

Executing the Allocation Efficiently on MT5

On the MT5 platform, you can find ETF CFDs in the Market Watch panel. Follow these steps for efficient execution:

- Search: Use the ETF’s ticker symbol to find the instrument.

- Size the Position: Calculate the money value of each trade as a percentage of your total account equity.

- Check Requirements: MT5 will show the contract value and margin requirement before you confirm the order.

- Use Limit Orders: Avoid market orders for less liquid assets. Use limit orders to control your entry price and reduce costs.

Risk Profile and Expected Performance Characteristics

Analyse how factor-tilted portfolios differ from standard benchmarks in terms of volatility, drawdowns, and the cyclical nature of investment styles.

Volatility, Drawdowns, and Tracking Error Versus Market Indexes

The Ben Felix portfolio will not closely follow a standard market-cap index. It will sometimes lead and sometimes lag, depending on how small-cap and value stocks perform. This difference is called tracking error.

Investors comparing their results to the S&P 500 every quarter will often see underperformance. This is expected. The factor investing strategies in this model historically require decades to succeed.

The maximum drawdown (the biggest drop from peak to bottom) will also differ from a standard index. Small-cap and value stocks often fall more sharply during crises, like in 2008 or early 2020.

More to Know:

2008 Financial Crisis: Small-cap value stocks fell harder than large-cap stocks as credit dried up for smaller firms.

Early 2020 Pandemic: The "Great Lockdown" caused a fundamental shock where value stocks (often in physical industries like travel or energy) crashed, while growth stocks (big tech) surged.

Value vs Growth Investing Cycles and Return Dispersion

Value vs growth investing describes the cycle between two styles:

- Value: Cheap stocks relative to earnings or book value.

- Growth: Companies with high expected earnings growth (like big tech).

These styles perform in alternating cycles. Between 2010 and 2020, growth stocks dominated. This caused the Ben Felix 5-factor portfolio to trail the market for a long time. However, value recovered sharply from 2021 onwards. This proves why you must stay disciplined rather than switching strategies based on recent trends.

More to Know:

Why Growth Won (2010-2020)? During this era, interest rates were near zero. When money is "free" to borrow, investors pay a premium for growth far in the future. As rates rose in 2021-2022, investors began demanding profits today, which brought the focus back to Value stocks.

Rebalancing and Long-Term Portfolio Discipline

Effective management involves using rules-based rebalancing and maintaining psychological resolve to stay committed to factor tilts during periods of underperformance.

Calendar vs Band Rebalancing Strategies

Rebalancing is the process of bringing your portfolio weights back to their original targets. Market movements cause these weights to “drift” over time. There are two primary ways to manage this:

- Calendar Rebalancing: You adjust your portfolio at fixed intervals, such as once every six months or once a year.

- Band (Threshold) Rebalancing: You adjust only when an allocation drifts from its target by a specified percentage (e.g., 5%).

Research from the Vanguard Investment Strategy Group suggests that band rebalancing can be more efficient. It ignores arbitrary dates and only acts when the “drift” is large enough to significantly change your risk level. This reduces unnecessary trades and can slightly improve your risk-adjusted returns.

Managing Market Beta and Currency Exposure

When you hold global ETFs, you face currency exposure. This is the risk that exchange rates change between your home currency and the fund’s currency. This adds a layer of volatility that is separate from the stock market.

Investors generally take two paths:

- Currency Hedging: Using hedged ETFs to remove exchange rate risk.

- Unhedged Exposure: Accepting currency swings, as they often balance out over long periods and avoid hedging fees.

Your choice depends on your time horizon and how much short-term volatility you can handle.

Market beta is your sensitivity to the general stock market. If your equity allocation drifts too far from your target, your market beta changes. This shifts your risk profile away from your original plan. Rebalancing is the only way to keep this risk consistent.

Maintaining Discipline During Extended Factor Drawdowns

The biggest psychological challenge of the Ben Felix portfolio is sticking to your “tilts” when they perform poorly. For example, the value factor trailed growth for over ten years after the 2008 financial crisis. Investors who removed their value tilt during those years missed the eventual recovery.

Discipline comes from understanding one truth: if a factor never underperformed, it would have no risk. If there is no risk, there is no risk premium. Underperformance is not a “bug” in the strategy; it is the very reason the extra return exists.

To stay on track, use a written investment policy statement. Review it once a year on a set date, rather than reacting to daily market news or stressful events.

Positioning the Ben Felix Portfolio Among Model Strategies

Evaluate how this academic framework compares to traditional market-cap indexing and how it integrates into the broader PWL Capital and Rational Reminder philosophy.

Comparison with Traditional Market-Cap Portfolios

A traditional market-cap portfolio holds companies in proportion to their size. It is low-cost, diversified, and historically outperforms most active managers after fees.

The Ben Felix portfolio builds on this foundation. Instead of replacing the market index, it adds systematic factor tilts (size, value, etc.) on top of it. This aims for higher long-term returns but comes with higher tracking error and periods where you will underperform the general market.

If you cannot handle seeing your portfolio lag behind the S&P 500 for several years, a simpler market-cap portfolio may be more appropriate for you.

| Feature | Market-Cap Index Portfolio | Ben Felix Factor Portfolio |

|---|---|---|

| Factor Exposure | Market beta only | Market beta + size, value, profitability, investment |

| Expected Return | Market return | Market return + factor premiums |

| Tracking Error | Minimal | Moderate to high |

| Fund Cost | Very low | Low to moderate |

| Difficulty | Low (Psychological) | High (During factor drawdowns) |

| Horizon | 10+ years | 15–20+ years |

Q: How does the “Internal Rate of Return” (IRR) typically differ between these two models over 20 years?

A: While a market-cap portfolio seeks to capture the “average” return of the economy, the Ben Felix model seeks “excess return” (Alpha) through higher risk-loading. Historically, a successful factor tilt can add between 0.5% to 2% to the annual IRR. While that sounds small, on a $100,000 investment over 25 years, a 1.5% difference can result in over $300,000 in additional final wealth due to the power of compounding.

Relationship to PWL Capital and Rational Reminder Allocations

The Ben Felix model portfolio is based on PWL Capital’s philosophy. They provide documentation on factor-tilted allocation, primarily for Canadian investors.

The Rational Reminder podcast provides the intellectual research for this construction. It covers the Fama-French five-factor model and the academic evidence behind these decisions.

While the funds Ben Felix suggests are often Canadian, the framework is global. Investors in other regions must adapt the specific fund selection to their own local taxes, regulations, and available ETFs.

Conclusion

Adopting the Ben Felix portfolio shifts you from a passive market passenger to an active harvester of academic risk premia. By moving beyond market-cap indexing, you are betting that smaller, cheaper, and more profitable firms will continue to reward those disciplined enough to hold them through any cycle.