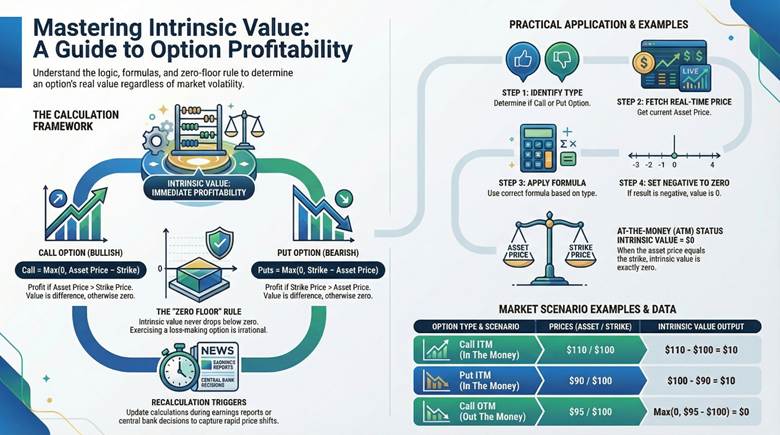

- Understanding the intrinsic value option helps traders distinguish between a measurable price advantage and speculative premium movements in volatile global markets.

- Applying the intrinsic value option formula consistently improves decision-making, especially when evaluating entry timing and expiration risk.

- Monitoring call and put intrinsic value supports smarter capital allocation by clarifying when real market positioning outweighs temporary pricing noise.

- Even with advanced calculators and AI tools, intrinsic value remains a foundational metric that grounds option strategies in objective price relationships.

Key Point:

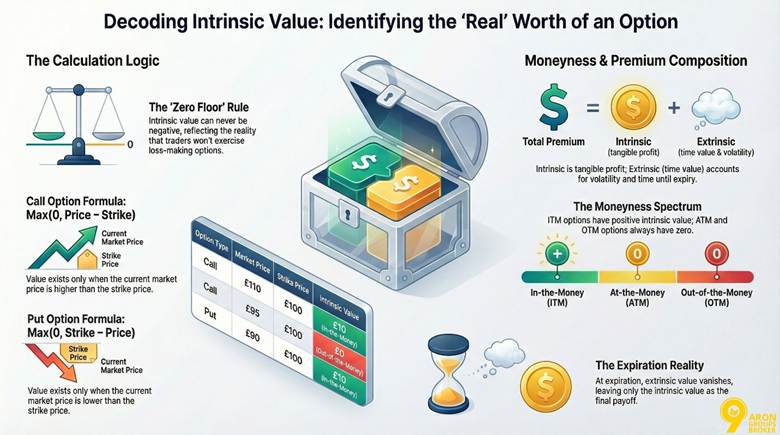

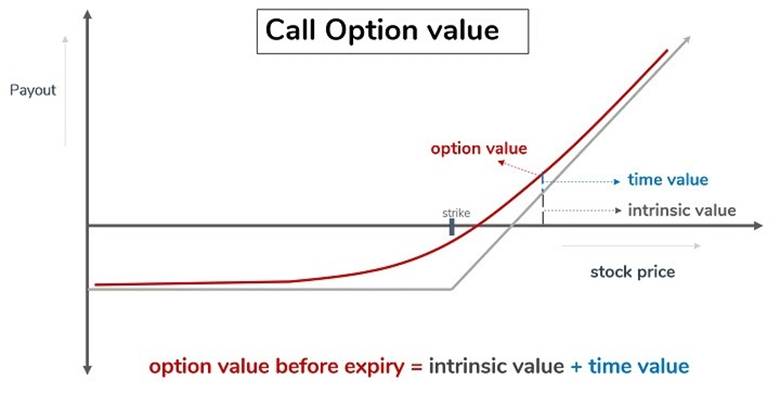

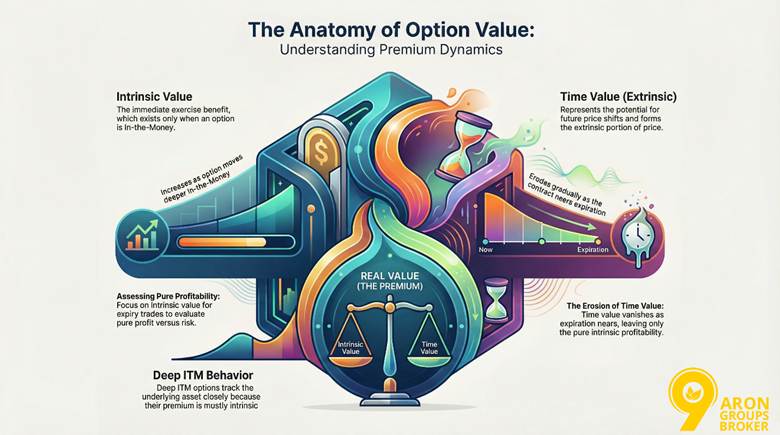

Intrinsic value ignores time decay, focusing solely on immediate exercise profitability—crucial for short-term trades.

More Info:

In volatile markets, intrinsic value can spike, but remember, options can expire worthless if OTM.

Key Insight:

Traders who monitor intrinsic value often protect their risk-reward structure, especially under pressure from emotions and trading psychology.

Did You Know:

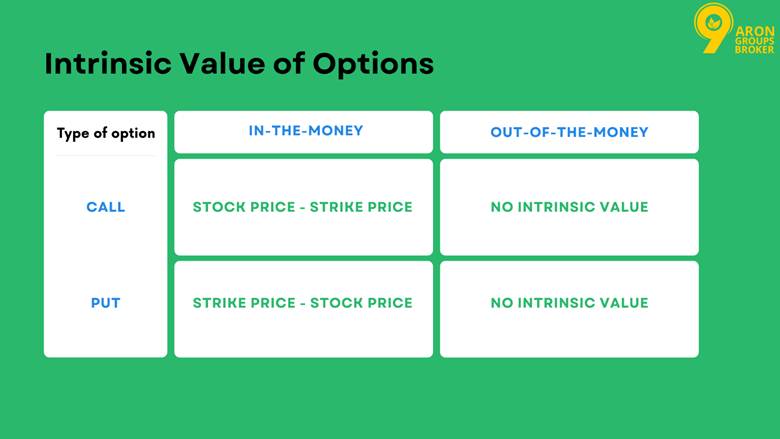

The Max(0, …) rule guarantees intrinsic value never goes below zero, matching real-world exercise decisions.

Note:

Calculators measure current value, but they do not forecast future direction. Combine outputs with fundamental analysis to judge whether price drivers support your thesis.

Key Point:

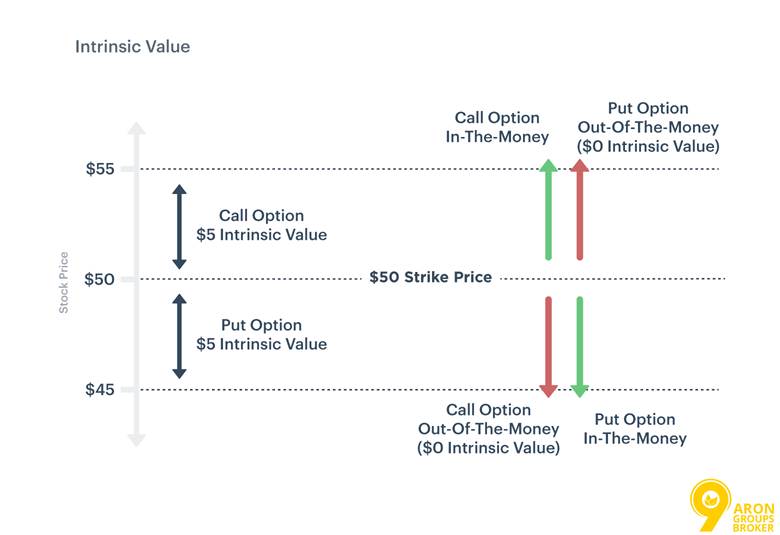

These examples show how small price changes can rapidly alter intrinsic value when the underlying trades near the strike.

More Info:

Favourable gaps signal buying opportunities, but assess premiums to ensure overall cost-effectiveness.

Key Insight:

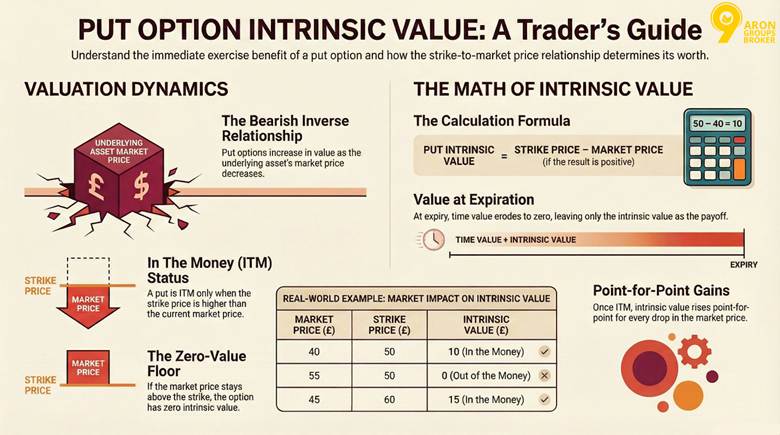

Puts are often used for hedging portfolio downside risk rather than pure speculation. Their protective value becomes evident during market stress, but timing remains critical.

Note:

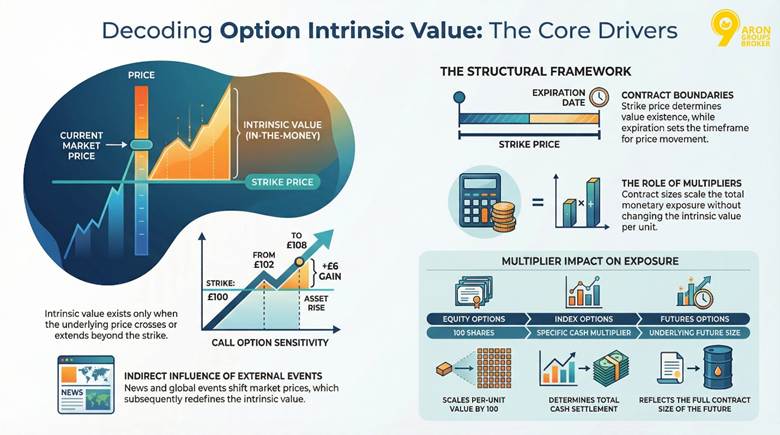

Even a small intrinsic value per unit can represent significant exposure when the contract size is large.

Key Point:

Focus on intrinsic for expiry trades, as time value vanishes, leaving only the Sharpe ratio-like efficiency in assessing pure profitability versus risk.

Warning:

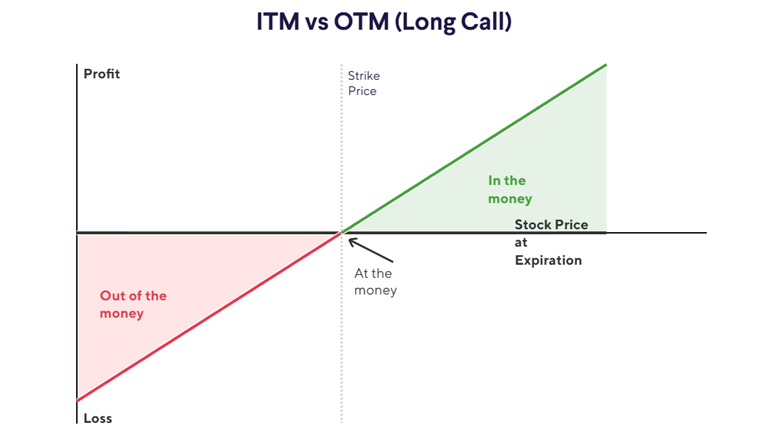

OTM contracts often appear inexpensive, but their probability of expiring without value is significantly higher.

Tip:

Before trading short-dated contracts, consider practising with a forex demo account to observe how moneyness shifts affect pricing in real time.