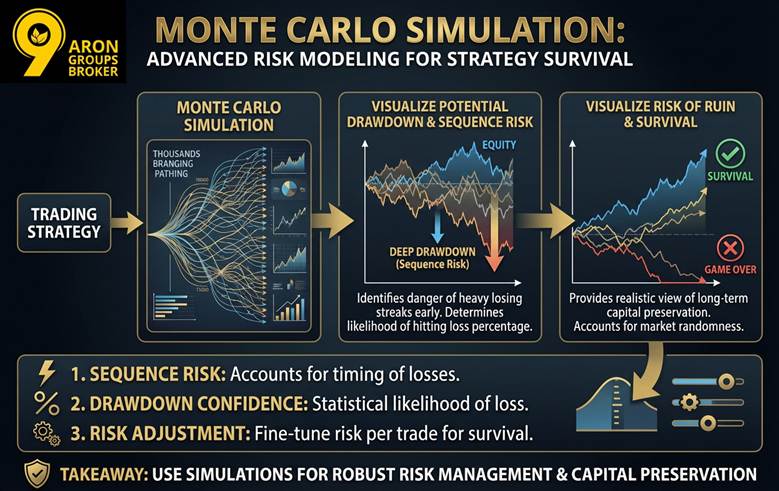

Key Points:

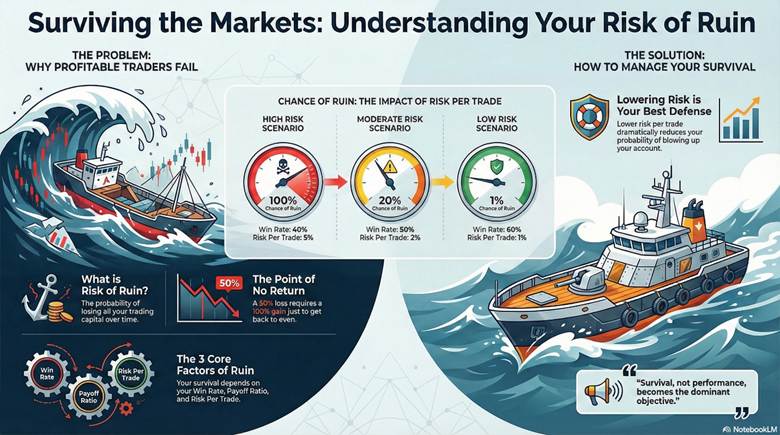

- Long-term survival in trading depends more on controlling risk exposure than on short-term profit or hit rate performance.

- The probability of ruin accelerates exponentially with higher risk per trade, making position sizing the most critical driver of survival.

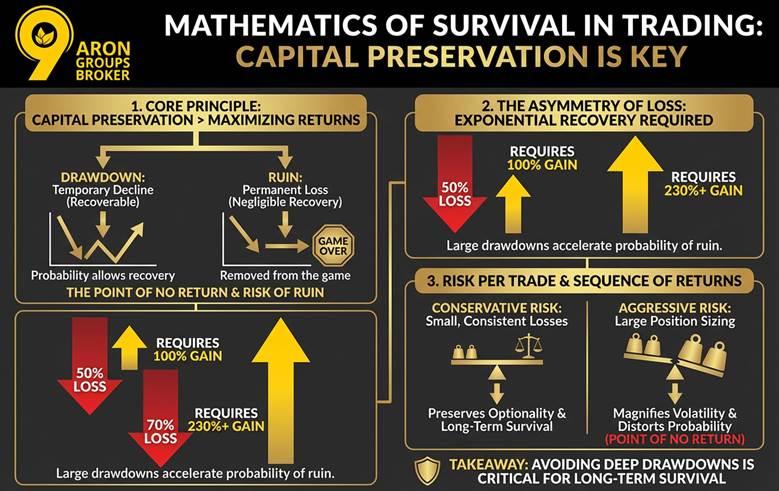

- The sequence of returns risk means identical statistical strategies can perform very differently depending on the order of wins and losses.

- Even with a positive edge (profitable strategy), failure to manage drawdowns can erase equity faster than historical backtests predict.

Did You Know?

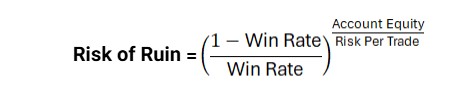

A strategy with a high win rate can still reach account ruin if losses are larger than gains on average.

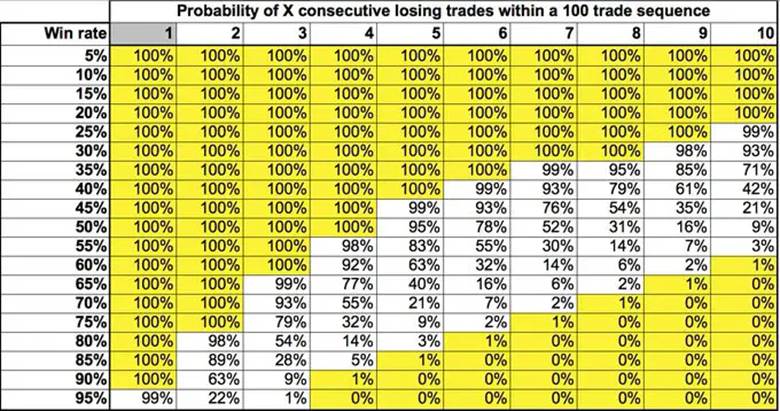

Risk of ruin does not increase linearly; once critical drawdown levels are reached, survival probability collapses rapidly.

Q: Does the risk of ruin table assume perfect execution?

A: Yes. Real-world errors often increase the actual probability of ruin beyond table estimates.

Key Insight:

A simple Excel formula can reveal hidden fragility in trading strategies long before losses become visible on the equity curve.