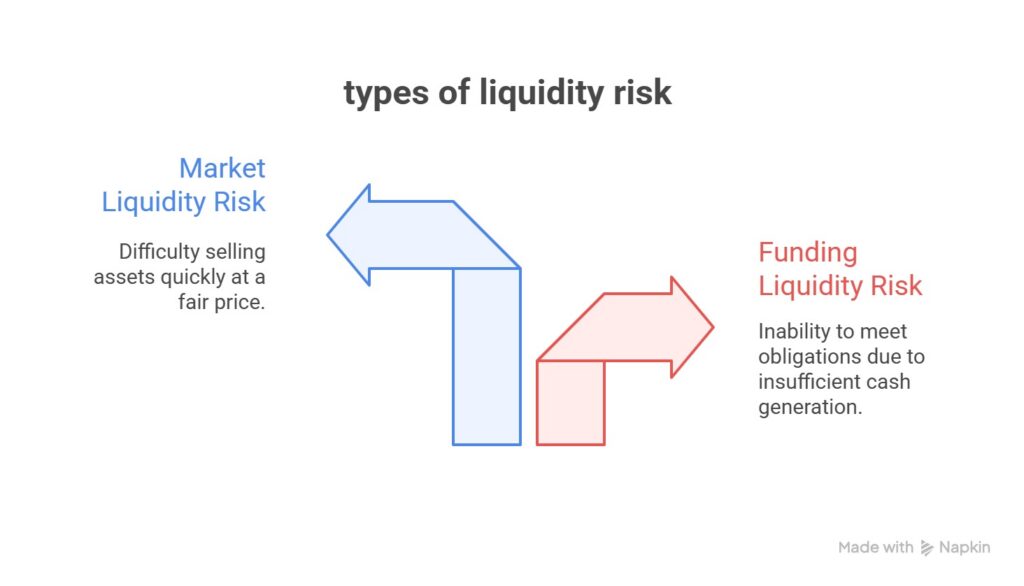

- Liquidity risk comes in two forms: funding liquidity risk (the inability to meet debt obligations) and market liquidity risk (the inability to sell an asset at a fair price).

- Banks are the most vulnerable to liquidity risk due to their maturity transformation model and heavy reliance on short-term deposits.

- In capital markets, low trading volumes, shallow market depth, and wide bid-ask spreads are the primary indicators of liquidity risk.

Factors such as economic recessions, macro-level financial crises, and a decline in public confidence in the banking system can trigger a wave of withdrawals, thereby amplifying liquidity risk in banks.

In 2023, fueled by panic amplified through social media, Silicon Valley Bank (SVB) in the United States faced a severe liquidity shortage as startups and tech companies simultaneously withdrew their deposits—ultimately leading to the bank’s collapse.

One of the most important tools for mitigating liquidity risk is the existence of regulatory and supervisory frameworks. By setting standards such as liquidity ratios, regulators not only help maintain the stability of the financial system but also safeguard depositors’ interests against potential crises.

Stocks with low trading volume and shallow market depth are more exposed to liquidity risk.

Large, actively traded stocks—such as those of index-leading companies—typically have very narrow spreads, while smaller or thinly traded stocks tend to carry wider spreads and pose higher liquidity risk.

Liquidity risk is not merely a threat to a bank’s balance sheet or an investor’s portfolio; if left unchecked, it can escalate into a widespread crisis capable of shaking the very foundations of the entire economy.

Basel III is an international regulatory framework for banks, developed in the aftermath of the 2008 financial crisis. Its goal is to enhance the stability and resilience of banks against financial shocks by setting stricter capital and liquidity requirements.