- Interest rate risk is a type of systematic risk that can only be mitigated through active risk management.

- A mix of swaps, options, futures, maturity diversification, laddered bond purchases, and counter-cyclical assets provides the strongest shield against interest rate shocks.

- Any change in interest rates can alter corporate borrowing costs and, consequently, their profitability.

- Rising or falling interest rates are not always just risks; for savvy investors, they can also create opportunities to rebalance portfolios and capture higher returns.

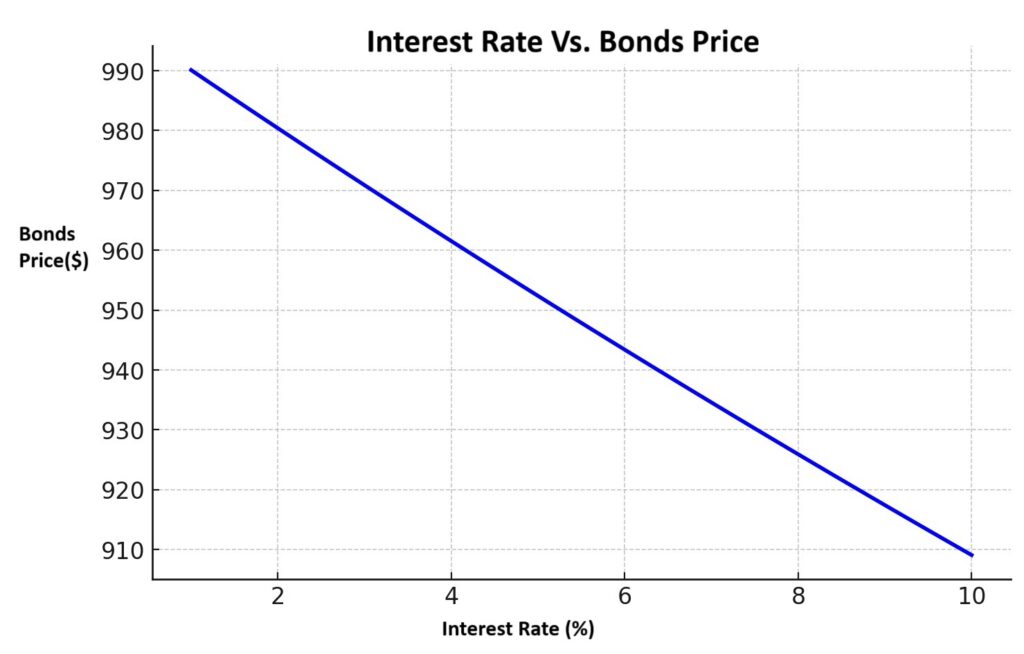

The reason behind the inverse relationship between interest rate risk and bond prices lies in the concept of opportunity cost. When interest rates rise, new bonds are issued with higher yields, making older bonds with lower rates less attractive to investors. As a result, the price of existing bonds must fall in order to remain competitive in the market.

The degree of a bond’s price sensitivity to interest rate changes is measured by an indicator known as Duration.

The LIBOR (London Interbank Offered Rate) was the average interest rate at which major international banks in London were willing to lend to one another on a short-term basis. For decades, it served as the global benchmark for pricing loans and financial instruments.

The SOFR (Secured Overnight Financing Rate), on the other hand, is based on actual transactions in the U.S. Treasury repurchase (repo) market—overnight loans collateralized by Treasury securities. It has been introduced as a more transparent and reliable replacement for LIBOR.

The factors driving interest rate risk can create volatility in the profitability of fixed-income investments. By understanding these factors and monitoring them closely, investors can develop more effective strategies to manage risk within their portfolios.

According to Investopedia, long-term bonds are generally more sensitive to interest rate changes and tend to experience larger price swings in response to rate fluctuations. To compensate investors for this added risk, a higher long-term yield—known as the Maturity Risk Premium—is typically offered.