- Track your total open risk daily, because correlation can exceed your per-trade rule without warning.

- Build a “risk downgrade” rule for bad sleep, stress, or rushed sessions, because execution quality drops.

- Use a fixed review ritual after loss limits, because reflection beats revenge trading every time.

- Avoid changing risk after a winning streak, because variance often reverses when confidence peaks.

Key Point:

If you cannot state the risk in cash terms before entry, you do not have a risk-per-trade rule.

Key Insight:

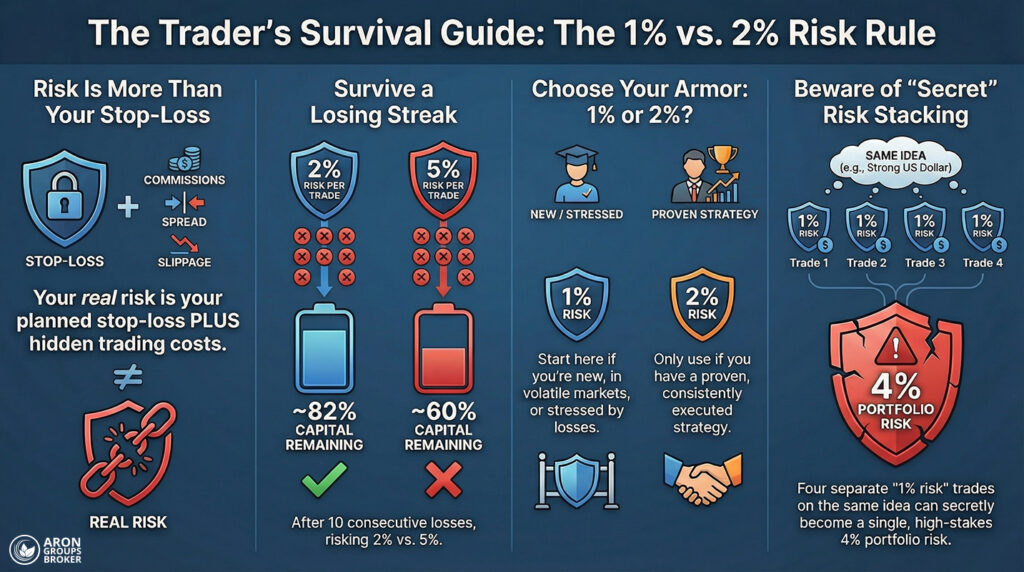

Correlation can turn “1% per trade” into 4% portfolio risk when multiple trades rely on the same idea.

More Info:

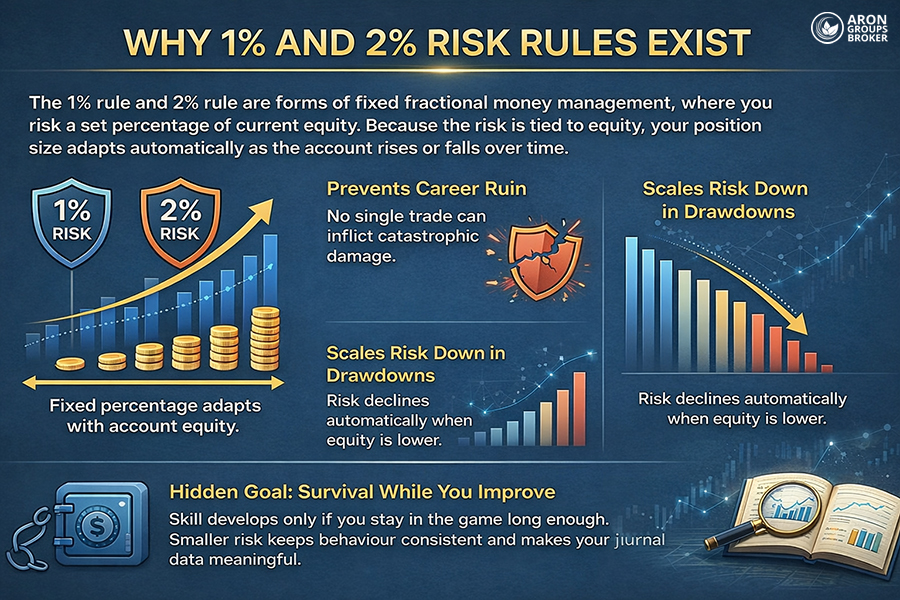

If your system is unproven in live conditions, start at 1% and earn 2% through stable execution.

Key Point:

Use 2% only if you can follow it after three losses in a row without changing the rules.

More Info:

Correlation can create a “streak” from one macro event, not ten separate decisions across independent ideas.

Key Insight:

Your edge needs time to express itself, and higher risk shortens the time you can stay consistent.

Key Point:

Budget a small friction buffer, particularly around news releases or thin liquidity, where spreads and slippage worsen.

More Info:

If two trades rely on the same USD move, treat them as one idea for sizing and cap the total risk accordingly.

Learn More:

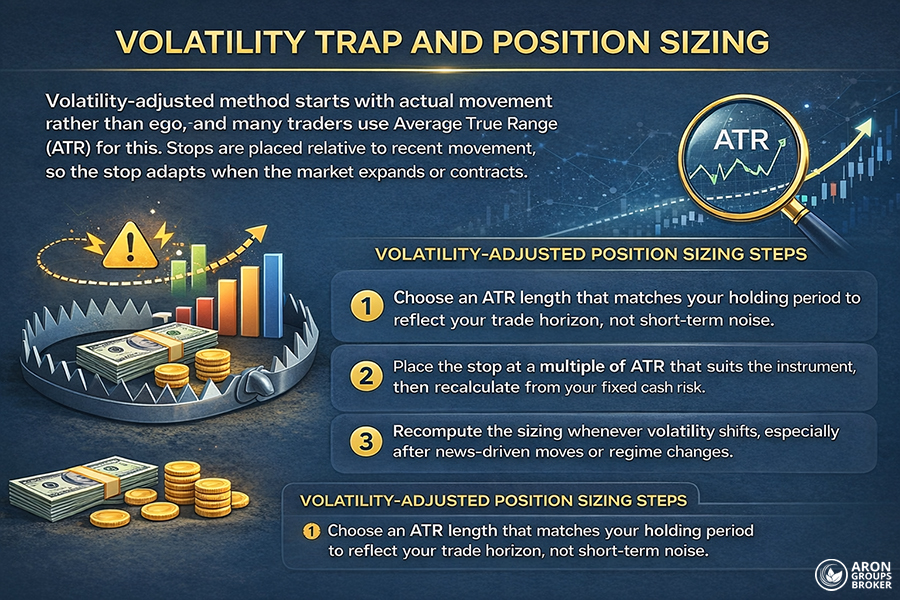

A risk per trade calculator is useful, but only if your stop distance and cost assumptions are honest.

Key Insight:

In gold and crypto, your stop method matters less than your resizing discipline when volatility expands suddenly.

Key Point:

If costs consume a large share of planned risk, change execution timing or stop structure before raising risk.

Key Insight:

Per-idea caps matter most during news-heavy weeks, when markets move as one system rather than separate charts.

Did You Know:

Many traders underperform backtests because they cannot maintain consistent sizing once stress and real losses arise.

Key Point:

Most blow-ups come from a short period of broken sizing, not from one bad trade.

Key Insight:

The best risk-per-trade calculator is the one you will actually use for every order.