- Most “fake” strategies are not scams; they fail because over-optimisation and curve fitting create fragile, non-repeatable backtest results.

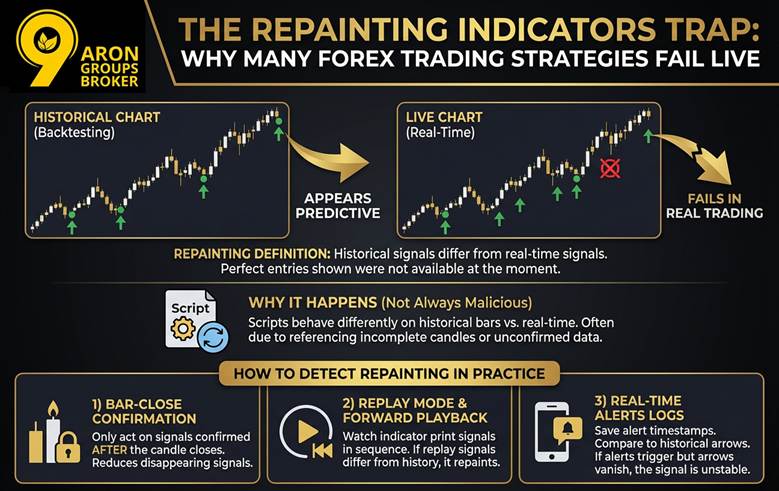

- Repainting indicators can rewrite history, so chart-perfect signals may never have existed in real time.

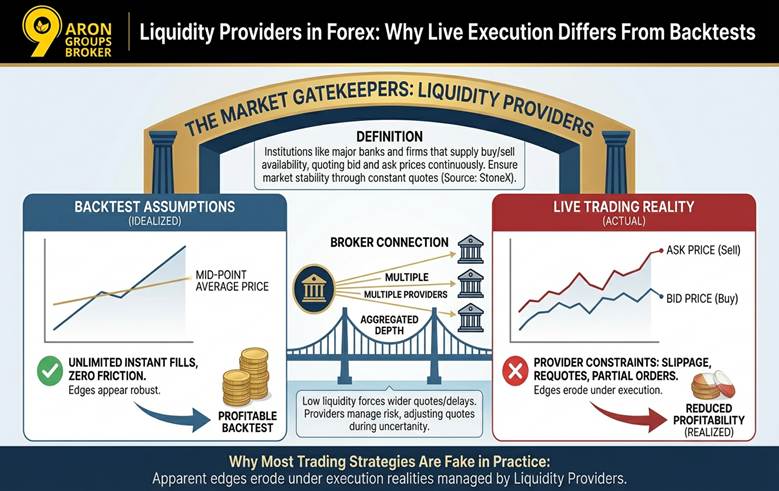

- Live execution is a gatekeeper: spreads, slippage, liquidity drops, and partial fills can erase small statistical edges.

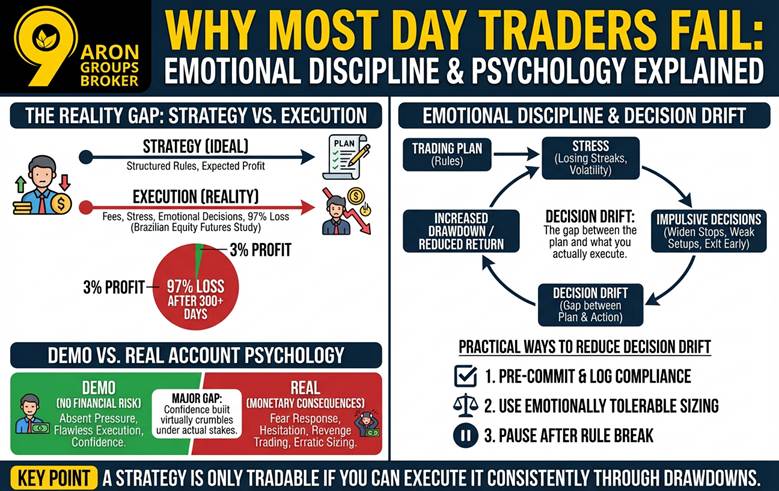

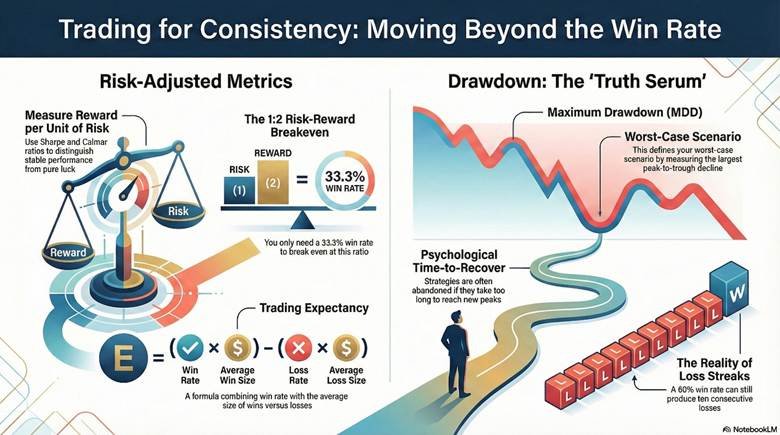

- Consistency is behavioural and risk-based: disciplined execution through drawdowns and risk-adjusted metrics matter more than win rate.

Did You Know:

Regulators consistently warn that many retail CFD accounts lose money due to leverage and product structure.

Key Point:

If small rule changes destroy results, the strategy likely has no stable edge.

Key Insight:

Repainting is not always malicious; it may result from how scripts use incomplete bars.

Key Insight:

Repainting is not always malicious. It can be a by-product of how scripts reference incomplete bars.

Practical check:

Re-run tests with worse spreads and realistic slippage. If profitability disappears, the edge is fragile.

Practical check:

Enforce bar-close logic and realistic order rules. Assume delayed fills and reject same-bar “magic” executions.

More Info:

The Deflated Sharpe Ratio was proposed to adjust performance for selection bias and backtest overfitting.

Key Point:

A strategy is only tradable if you can execute it consistently through drawdowns.

Key Point:

Focusing on risk-adjusted metrics prevents you from being blinded by the "perfect" equity curves often used to market fake strategies.

Did You Know?

Regulators frequently highlight that leveraged derivatives can amplify losses rapidly, making drawdown control the central pillar of long-term survival.