Key Takeaways

- De-dollarization is a structural tailwind for gold: reserve managers replacing dollar assets overwhelmingly choose bullion.

- Central banks bought 863 tonnes in 2025 and an estimated 244 tonnes in Q1 2026; the World Gold Council expects about 850 tonnes for the full year.

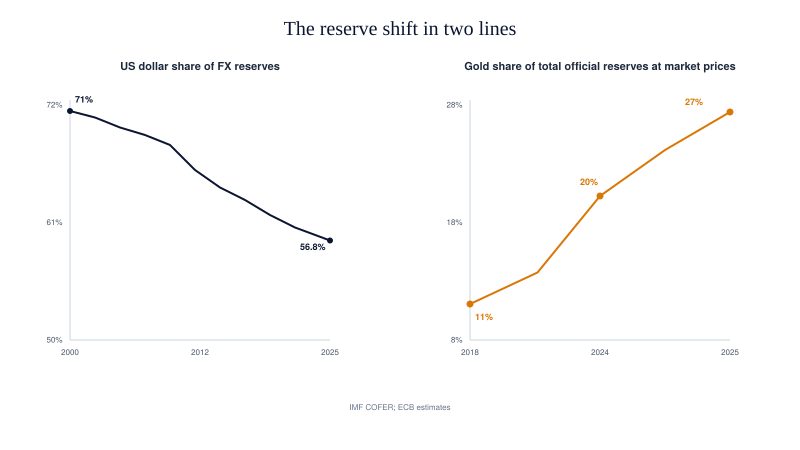

- Gold reached about 27 percent of global official reserves at end-2025, overtaking US Treasuries, while the dollar's share of FX reserves slipped to 56.8 percent.

- The gold-dollar link is usually inverse, but real yields and Fed policy can dominate it for months at a time.

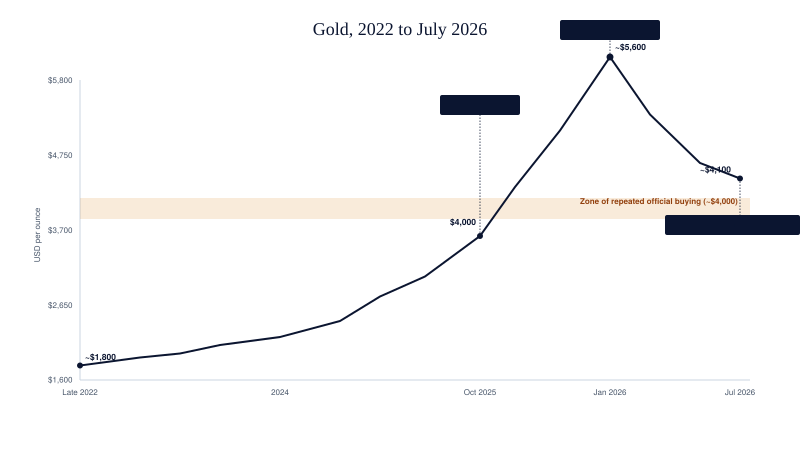

- The 2026 correction, gold's worst quarter in 13 years, proves the theme is structural, not a one-way price guarantee.

- Active traders express the theme most directly through XAU/USD CFDs, where leverage demands strict risk control.

Risk Disclosure

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Past performance is not indicative of future results. This content is provided for educational purposes only and does not constitute investment advice.

Did You Know?: The ECB estimates gold ended 2025 at roughly 27 percent of global official reserves at market prices, overtaking US Treasuries at about 22 percent for the first time. Total official holdings, near 36,000 tonnes, sit close to the 1965 record. |

Rule: The theme sets the bias; the level and the stop set the trade. |