- Serial correlation can inflate the Sharpe ratio unless you adjust for the standard error.

- Negative skew can matter more than volatility for tail-heavy strategies.

- Stability across regimes matters more than the best historical ratio value.

- Return smoothing can improve ratios while hiding liquidity and gap risk.

Key Point

Risk-adjusted metrics compare fairly only when returns and risk use the same sampling frequency.

Did You Know

Many proprietary trading challenges fail traders due to drawdown rules, not low returns.

More Info

A benchmark mismatch can convert market exposure into skill on paper, especially in short samples.

Key Insight

A Sharpe ratio can rise when returns look smoother, even if rare losses grow larger.

Did You Know

Sortino ratios are comparable only when the same MAR is used for all strategies.

Key Point

Calmar can collapse after one crisis week, even if the strategy’s expected return remains similar.

More Info

If the benchmark is too easy, information ratios inflate and hide the true opportunity cost.

Key Insight

If your average loss is unbounded, ratios can look acceptable until a single trade wipes out months of progress.

More Info

If funding rules allow a 5% drawdown, your hurdle rate should reflect the limited-risk budget.

Key Point: Capital is frequently the binding constraint on a strategy, even when the market opportunity appears exceptionally large.

Did You Know:

Ratios based on simple equity changes can differ from log-return calculations, especially in volatile markets.

Pro Tip:

If you set MAR = 0, Sortino becomes a loss-focused efficiency metric that suits drawdown-limited trading.

Did You Know:

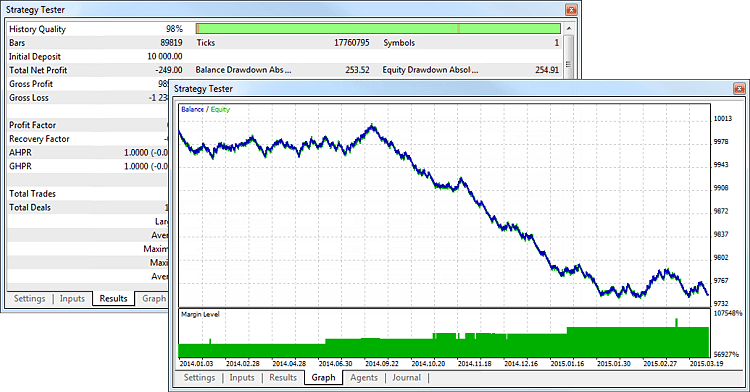

A backtest may appear stable, but it can lose its high Sharpe ratio once realistic slippage is applied.