Direct indexing has moved from an institutional niche to a mainstream strategy, and the range of providers has expanded sharply as a result. Minimums that once started above a million dollars now begin as low as a few thousand. Fractional share trading makes precise index replication viable at virtually any account size.

The appeal is straightforward: instead of owning a fund that tracks an index, the investor owns the underlying securities directly. That distinction enables security-level tax-loss harvesting, portfolio customisation based on ESG criteria or sector exclusions, and tighter control over the tax consequences of every position.

This guide explains how direct indexing works in practice, compares the leading providers on fees, minimums, and services, and identifies the strategies that add genuine value rather than complexity.

- Direct indexing means owning individual securities rather than fund shares, which enables security-level tax-loss harvesting.

- Tax alpha is the additional after-tax return generated by offsetting gains with harvested losses; it compounds over time.

- Minimums have fallen significantly, with some providers now starting below $5,000.

- Fractional shares allow full benchmark replication without needing large capital to buy every constituent.

- ESG integration and sector exclusions are straightforward in a direct account but require careful tracking and error management.

- Fees vary widely; some providers charge separately for the direct indexing layer on top of underlying asset management costs.

- Tracking error can widen materially during customisation if position counts drop too far below the benchmark.

Understanding Direct Indexing Providers

Direct indexing providers sit between the investor and the market, handling the operational complexity of owning hundreds of individual securities instead of a single fund. The provider manages portfolio construction, automated rebalancing, tax-loss harvesting, and compliance with the investor’s personal constraints.

What separates one provider from another is not the concept itself but the quality of execution: how precisely the portfolio tracks its benchmark, how intelligently the algorithm harvests losses, and how much flexibility the investor retains over customisation. This section covers the core mechanics before comparing specific platforms.

What Direct Indexing Providers Offer

A direct indexing provider manages a separately managed account (SMA) that holds the individual securities constituting a chosen index or benchmark. The provider handles rebalancing, dividend reinvestment, and tax-loss harvesting automatically, adjusting the portfolio to track the benchmark whilst responding to the investor’s personal constraints and tax situation.

The core services differ from a standard fund in three important ways:

- The investor appears as the named owner of each security, which creates direct legal and tax ownership.

- Losses on individual positions can be realised and used to offset gains elsewhere without triggering a fund-level taxable event.

- Specific stocks can be excluded or overweighted based on personal preferences, company exposure, or employer stock concentration concerns.

Direct indexing providers manage over $700 billion in assets globally, with growth accelerating since fractional share trading became widely available.

Tax Alpha and Security-Level Tax-Loss Harvesting Explained

Tax alpha is the improvement in after-tax returns from actively realising losses on individual positions whilst maintaining overall market exposure. Fund investors cannot harvest individual constituent losses. They do not own the underlying shares.

In a direct indexing account, the provider sells a declined stock, books the loss, and replaces it with a correlated security during the wash-sale window. Over a full market cycle, this process compounds into meaningful tax savings.

For a detailed explanation of wash-sale rules and their effect on harvesting strategies, see the IRS Publication 550 guidance on investment income and expenses.

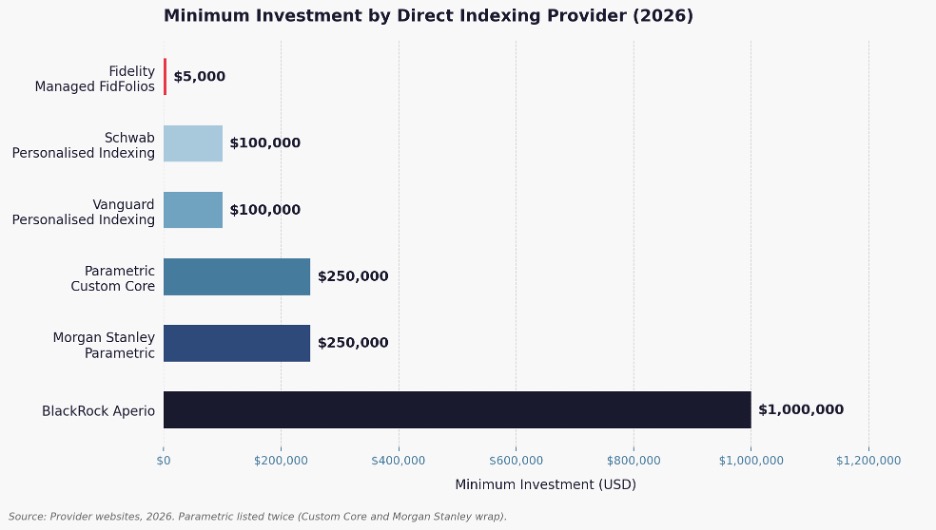

| Provider | Minimum | Annual Fee | Benchmark Options | Fractional Shares |

|---|---|---|---|---|

| Fidelity Managed FidFolios | $5,000 | 0.40% | S&P 500, US Total Market | Yes |

| Schwab Personalised Indexing | $100,000 | 0.20%–0.35% | US, International, Blended | Yes |

| Vanguard Personalised Indexing | $100,000 | 0.20%–0.35% | US, International, Blended | Yes |

| Parametric Custom Core | $250,000 | 0.25%–0.40% | Wide range incl. factor tilts | No |

| Morgan Stanley Parametric | $250,000 | Variable | Global, ESG, factor | Limited |

| BlackRock Aperio | $1,000,000 | Negotiated | Full global menu | Yes |

Fidelity

Fidelity’s Managed FidFolios entry point at $5,000 is the lowest among major custodians and represents a genuine change in accessibility. The programme uses fractional shares to replicate the S&P 500 or the total US market without requiring large capital to buy every constituent.

The 0.40% annual fee is competitive at the lower end of the account size range. It does not decrease at higher balances in the way some rivals structure their pricing. Harvesting runs daily, which maximises the number of opportunities captured in volatile markets.

The limitation is that the benchmark menu is narrower than that of specialist providers, and international exposure is not available as a standalone direct indexing option.

Read More: What is tax-loss harvesting?

Schwab

Schwab Personalised Indexing ($100,000 minimum, 0.40% fee) allows ESG screening, sector exclusions, and individual stock restrictions with daily harvesting. It integrates well within the Schwab custody ecosystem, whilst its fee structure bundles advisory and indexing costs in a way that makes direct price comparisons difficult.

Vanguard

Vanguard Personalised Indexing stands out on cost. The 0.20% starting rate for simpler mandates is the lowest among major custodians offering genuine daily harvesting, reflecting Vanguard’s historical cost discipline.

The minimum is $100,000, and the service is delivered through Vanguard’s advisory platform rather than as a self-directed product.

Parametric

Parametric, owned by Morgan Stanley, remains the benchmark for institutional-grade direct indexing. The $250,000 minimum reflects a more sophisticated service that includes factor tilts, concentrated stock management, and global benchmark coverage that retail-oriented platforms do not offer.

The technology behind Parametric’s harvesting and rebalancing is more mature than most rivals, and the firm holds the longest institutional track record of measured tax alpha. The higher minimum and variable fee structure make it less appropriate for the lower end of the high-net-worth market.

Fractional Share Trading and Benchmark Replication

Fractional shares are what make direct indexing viable below $500,000. Without them, replicating the S&P 500 in full would require far more capital than most retail investors hold. A $10,000 account can now hold proportional exposure to all 500 constituents.

Providers with native fractional infrastructure achieve better replication accuracy, particularly at lower account sizes where individual share prices represent a larger proportion of total capital. As account sizes rise, the need for fractional shares decreases and tracking error from other sources — such as exclusions or factor tilts — becomes the dominant concern.

Direct Ownership of Securities: Why It Matters

As the shareholder of record, the investor controls each position individually. That means appreciated shares can be donated to charity to eliminate capital gains on those positions, shares can be tendered in an acquisition on individual terms, and specific holdings can be excluded without affecting any other investor’s account. In a fund, none of this is possible. The custodian — not the investor — holds the securities.

Read More: What is a separately managed account (SMA)?

Evaluating Providers: Fees, Minimums, and Services

When choosing a direct indexing provider, it is important to look past the advertised fee. The quoted price may include advisory services, custody, or financial planning — or it may not. Some providers offer a single bundled fee based on assets under management; others add direct indexing as an extra service layer on top of an existing advisory relationship.

Other important factors include how well the provider manages tracking error, the depth of ESG integration, and the sophistication of the tax-loss harvesting algorithm. This section covers the criteria that separate good providers from great ones.

Comparing Costs and Account Minimums

The quoted fee is not always the full cost. Some providers charge a direct indexing overlay on top of advisory fees; others bundle everything into a single AUM rate. Always confirm whether the fee covers only portfolio management or also includes financial planning and custody.

Q: Does fee compression in direct indexing reflect commoditisation?

A: Yes, partially. Tax-loss harvesting has become standardised and technology costs have fallen. Retail fee pressure is real. Specialist providers justify higher fees through execution quality, global coverage, and factor integration — not the harvesting function itself.

Tracking Error Management Explained

Tracking error is the difference between a portfolio’s returns and the benchmark’s returns. Some deviation is expected because substitutes are held during wash-sale windows, exclusions permanently remove names, and practical trading creates drift.

The practical ranges are approximate, not guarantees. Light customisation typically targets low tracking error, whilst heavier exclusions and factor tilts increase it — sometimes materially. When tracking error rises beyond an acceptable threshold, the portfolio begins behaving as a distinct strategy rather than an index-like holding.

Tracking error below 1.00% per year is generally acceptable — tax and customisation benefits outweigh benchmark deviation at this level. Above 2.00%, the portfolio's behaviour diverges enough to create meaningful return variance relative to the index.

Customisation and ESG Integration Options

ESG integration typically works through exclusion screens: remove tobacco, weapons, or fossil fuels without exiting the broader index. Vanguard and Fidelity apply third-party ESG ratings at the individual company level. Parametric and Aperio offer more granular control, including revenue threshold screens — for example, excluding companies deriving more than 5% of revenue from a specific activity.

Beyond ESG, customisation can extend to include the following options:

- Factor tilts toward value, quality, or momentum.

- Position caps on individual names to limit single-stock concentration.

For an overview of ESG screening methodologies, see the CFA Institute’s ESG investing research and standards.

Advanced Direct Indexing Strategies

Once the basics of direct indexing are in place, the real value comes from execution quality and strategic refinement. Daily harvesting algorithms, volatility-driven loss capture, and cross-account tax coordination can meaningfully increase after-tax returns over a full market cycle.

Advanced strategies also involve managing the tension between customisation and tracking error. Heavy exclusions or factor tilts push the portfolio further from its benchmark, and the tools for managing that divergence differ significantly across providers.

Maximising Tax-Loss Harvesting Benefits

Daily harvesting algorithms capture losses the moment positions cross a threshold, sell, replace with a correlated security, and book the loss immediately. Quarterly or monthly harvesting misses short-lived declines that recover within weeks.

The annual harvest volume is tightly linked to volatility. A flat, rising market produces few individual-stock losses. A year with heavy sector rotation can produce five to ten times as many harvesting events. Tax alpha should always be evaluated across a full market cycle, not a single year.

From Monday morning in Australasia to Friday afternoon in New York, You can trade in the forex market. One of the most important reasons traders love Forex is that it does not close overnight, so it is not important where you are or what time it is; you can always trade Forex because it is always open somewhere in the world.

Using Tax Alpha to Improve After-Tax Returns

Tax alpha is most valuable for investors in high tax brackets with regular capital gains realisations from other sources. A business owner selling equity stakes, a real estate investor with recurring property gains, or an executive receiving stock compensation can use direct indexing losses to systematically offset these gains.

Taxes deferred today remain invested and generate returns. Over a decade, deferring even modest annual tax bills can add meaningful after-tax wealth relative to a fund-based approach that does not offer the same harvesting capability.

For a detailed comparison of direct indexing versus ETF-based approaches on an after-tax basis, see the Vanguard research on direct indexing and tax efficiency.

Reducing Tracking Error Whilst Customising Portfolios

Customisation and tracking error move together: more exclusions mean more deviation. Three tools help manage that tension without abandoning the index character of the portfolio:

- Sector-neutral substitution: replace excluded stocks with sector peers to preserve sector weights.

- Factor constraints: apply factor tilts on the remaining portfolio to maintain intended exposure.

- Sector deviation limits: cap drift from benchmark weights at a defined tolerance.

Institutional providers such as Parametric and Aperio run optimisation algorithms against these constraints. Retail-oriented platforms typically apply simpler rules that widen tracking error more quickly under heavy customisation.

Q: At what point does customisation begin to undermine the index character of a direct indexing portfolio?

A: When tracking error consistently exceeds 2.00% annually, the portfolio’s return profile diverges meaningfully from the benchmark. At that level, the investor should assess whether the customisation benefits — tax savings, ESG alignment, or concentration management — justify the deviation, or whether a different portfolio structure would serve the objective more efficiently.

Choosing the Right Direct Indexing Provider

The decision on which provider to use depends on account size, tax complexity, and the level of customisation required. A retail investor with a $10,000 account has different needs from a family office managing concentrated stock positions. The two situations call for fundamentally different platforms.

This section provides practical guidance on matching the right provider to the right situation, including recommendations for each account size tier.

Key Factors Beyond Fees and Minimums

The minimum and headline fee are starting points. The factors that determine real-world outcomes are more granular and often surface only after implementation:

- Harvesting frequency and algorithm sophistication: daily is meaningfully better than weekly or monthly.

- Cross-account wash-sale monitoring: failure here invalidates losses and creates unexpected tax bills.

- Tax report quality: lot-level detail and substitute security tracking are non-negotiable in complex situations.

Ask providers specifically how they handle wash sales across multiple accounts in the same household. This is where most retail-oriented platforms have real limitations. Request a sample tax report before committing; if it does not show lot-level detail and substitute security tracking, the reporting quality may be insufficient for complex tax situations. Also confirm whether the provider’s tracking error figures are live results or back-tested estimates, as back-tested figures frequently overstate real performance.

Expert Recommendations on Top Providers

Under $100,000: Fidelity FidFolios. Daily harvesting, fractional replication, and the lowest minimum in the market. The 0.40% fee outperforms pure index funds on an after-tax basis for investors in the 32% bracket and above during volatile years.

Between $100,000 and $250,000: Vanguard Personalised Indexing. The 0.20% base fee is the best cost-to-quality ratio among custodians offering genuine daily harvesting, with adequate benchmark coverage for most standard mandates.

Above $250,000 with complex needs: Parametric. Factor tilts, global coverage, concentrated stock management, and the longest institutional track record of measured tax alpha justify the fee premium.

Aron Groups: Flexible Alternative to Institutional Gatekeepers

Aron Groups provides direct indexing access outside the major custodian ecosystem, with no requirement for an existing advisory relationship. The platform serves investors with custodial relationships at smaller broker-dealers or family offices who need institutional-grade tax management without migrating assets to a large platform. It is particularly suited to investors whose account structure, mandate complexity, or broker-dealer relationship does not fit the standard minimum and service tiers of the major custodians. The onboarding process is designed to accommodate non-standard mandates without the constraints typically associated with large-platform programmes.

Read More: How to get started with direct indexing at Aron Groups

Future Trends in Direct Indexing

The next generation of direct indexing will likely include real-time fractional replication, dynamic ESG scoring, and estate planning integration. This section covers the developments that will shape the market over the next three to five years.

Innovations in Fractional Share Trading and Benchmark Replication

The next phase is real-time fractional replication: continuous weight adjustment as dividends are reinvested, rather than weekly or monthly batching. International direct indexing is also expanding as a category, though settlement differences, foreign tax treatment, and currency management remain obstacles for most providers.

Trends in ESG Integration and Portfolio Customisation

Binary exclusions are giving way to dynamic ESG scoring. Continuous ratings tilt weights towards higher-scoring companies within each sector rather than removing the sector entirely. This reduces tracking error whilst still lowering average ESG risk. Personal values screens are expanding into supply chain standards, human rights metrics, and political contribution data, though third-party rating quality remains uneven.

Anticipated Changes in Fees, Minimums, and Tax Strategies

The 0.40% standard fee is expected to move towards 0.20%–0.25% for standard mandates over the next three to five years. Minimums will continue to decline — from above $1 million a decade ago to $5,000 today — with zero-minimum standard-benchmark products a credible near-term possibility.

Tax strategy is also expanding into estate planning. Step-up-in-basis management identifies high-gain positions to hold until death rather than harvest during the investor’s lifetime, combining the benefits of direct ownership with long-term estate efficiency.

Conclusion

Direct indexing delivers real after-tax advantages for investors with meaningful capital gains exposure or complex customisation needs — provided the provider, fee structure, and harvesting technology match the investor’s actual situation. Fees are falling, minimums are declining, and benchmark coverage is widening. Investors entering today through Fidelity or Vanguard are accessing infrastructure that was reserved for institutional mandates until very recently.

The decision between providers ultimately comes down to where complexity arises. Standard accounts with broad-market mandates are well served by the major custodians. Accounts with concentrated positions, factor requirements, or multi-account tax coordination benefit from specialist providers such as Parametric or Aperio. Matching the platform to the actual need is where the meaningful advantage is found — not the decision to use direct indexing in the first place.

FAQ

What Are Normal Tracking Error Levels for Direct Indexing Providers?

Standard large-cap mandates with limited customisation should sit below 0.50% annually. Excluding 20 to 30 or more constituents typically pushes this to 0.75%–1.50%. Aggressive exclusions or factor tilts can exceed 2.00%, creating meaningful return variance versus the benchmark.

When Does Tax-Loss Harvesting Add Little Value?

Harvesting adds little value for investors in the 15% bracket or below, in low-dispersion rising markets, or when there are minimal gains to offset. Retirement accounts gain nothing from harvesting since they are already tax-deferred. The strategy is strongest for high-bracket investors with regular taxable gains from business sales, property, or equity compensation.

What Should You Check First: Wash Sales, Rebalancing, or Cash Handling?

Start with cross-account wash-sale monitoring; it is the most common source of tax errors in multi-account households. A provider that harvests a loss and repurchases the same security within 30 days in another account at the same custodian invalidates that loss. Then review rebalancing methodology and whether the provider invests contributions and withdrawals on a tax-aware basis.

Why Do Portfolios Tracking the Same Benchmark Behave Differently?

Algorithm differences in timing, loss thresholds, and substitute security selection create divergence even between accounts with the same mandate. Cost basis path dependence also matters. Accounts opened on different dates accumulate different gain and loss profiles, driving different harvesting patterns over time.

Is Direct Indexing Worth It for Buy-and-Hold Investors?

For investors who hold indefinitely and donate appreciated positions to charity, the harvesting benefit is limited; the step-up in basis at death achieves similar deferral without active management. The stronger case is customisation: ESG screening, employer stock exclusion, and concentration management are valuable regardless of tax bracket or how often gains are realised.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Past performance is not indicative of future results. This content is provided for educational purposes only and does not constitute investment advice.